Experience Curves, Declining Cost Incrementality & Extreme-Value Pricing Strategies

Incremental costs that are typically lower than average costs will decline even further with unit sales, increasing the potency of extreme-value pricing strategies.

While reading Jean-Manuel Izaret and Arnab Sinha’s excellent new book, Game Changer: How Strategic Pricing Shapes Businesses, Markets, and Society recently (I strongly recommend it), I came across a concept I hadn’t encountered in a while: the experience curve. An experience curve (also known in the organizational behavior/ strategy literature as a learning curve, e.g., Argote & Epple, 19901) is the idea that with accumulating production, the costs of producing decline by a constant percentage with each doubling of cumulative production. After their heyday in the 1980s, experience curves have faded into the background of most pricing strategy discussions.

Izaret and Sinha’s brief but insightful treatment of experience curves got me thinking about one application of experience curves that every pricing decision-maker should know about: their implications for the efficacy of extreme-value pricing strategies. In a nutshell, any product or service that is subject to significant experience curve-driven cost declines, whether they are incidental or deliberately designed into the offering, should favor using extreme-value pricing strategies such as blowout price promotions or appreciably low, all-in prices to accelerate that ride down the curve. In this post, I want to build out this argument, refreshing your thinking about the experience curve along the way.

A brief primer on experience curves

An experience curve is the hypothesis that for any seller, as the cumulative production increases, the average costs decline systematically (Day & Montgomery, 1983). By 1985, thousands of studies across various industries found a decline in production costs of 10%-30% for every doubling of cumulative production for everything from Model T Fords to titanium dioxide and dynamic RAM chips (Ghemawat, 1985)2. The flurry of studies showing experience curve effects continues to this day.

Along with Porter’s Five Forces and C. K. Prahalad’s Market Pyramid, the experience curve was deemed as “one of the charts that changed the world” by Harvard Business Review in 2011 because of the significance of the idea that businesses enjoy sustained competitive advantage conferred by experience curves. As companies produce more of a product or service, they become more efficient at making it and also innovate through redesigning, multi-purposing, and upgrading technology, all of which lead to continued lowering of costs and an advantage over competitors.

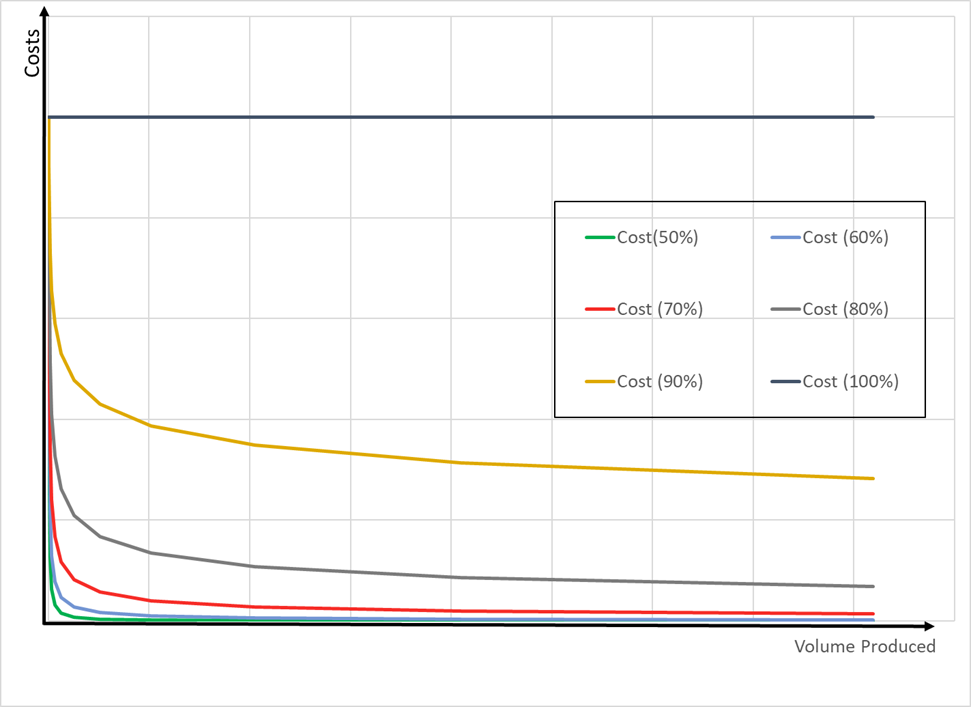

Graphically, an experience curve can be shown using either of the following two graphs. The first graph shows experience curves depicting different rates of declining costs using raw data, while the second graph uses log scales to show the same data. (Experience curves are conventionally shown on log scales).

In both figures, a 100% cost curve is the horizontal line, indicating that costs do not vary with cumulative production. In contrast, a 50% experience curve means that for every doubling of cumulative production, the costs will decline by half. We can also distinguish between cost experience curves that investigate and exploit the decline in costs and price experience curves that track the decline in prices and exploit this information for forecasting and pricing. Here, our focus is on cost experience curves.

I should note there are numerous criticisms of experience curves in the academic literature. In the 1980s, there was a lot of back-and-forth between various scholars about issues such as how experience curves can be used and misused for strategic decisions. Regretfully, that highly interesting discussion is beyond the scope of this post.

Izaret and Sinha’s (2023) ideas about cost experience curves

In their Game Changer book, Izaret and Sinha discuss cost experience curves (they call them the “BCG slope of a cost curve”) in the context of cost-plus pricing3. Instead of considering the reduction in average costs that occurs with cumulative production, the authors separately consider how fixed, variable, and semi-variable costs change as a function of the number of units sold. Their main goal is to develop precise estimates of costs to use in a cost-plus formula.

As shown in the figures above, a purely variable cost, such as the food cost at a restaurant or the cost of t-shirt blanks for a streetwear label, does not scale down with the number of units sold. Purely variable costs are the same for the first unit sold, for the 1000th unit sold, and for the millionth unit sold; they fall on the 100% experience curve. On the other hand, no costs scale down as much as a purely fixed cost. Purely fixed costs like the restaurant’s rent or the streetwear brand’s t-shirt printing equipment fall on a 50% experience curve. A doubling of units sold will halve the fixed cost per unit, a quadrupling will quarter it, and so on.

Another useful thing Izaret and Sinha point out is that most costs are semi-variable in practice rather than purely fixed or purely variable. For instance, both food costs and t-shirt blank costs can enjoy quantity discounts which makes them semi-variable, not purely variable. Similarly, rent can be negotiated down if a restaurant is very popular and draws business to other tenants, making it dependent on units sold, and thus semi-variable.

The authors suggest that costs typically fall on anywhere between 60% and 90% experience curves, meaning there is a reduction of 10-40% in most costs for every doubling of units sold. Thus, incremental costs are not only lower than average costs, but they are subject to what I call declining incrementality from experience curve effects.

The main insight I took away from the authors’ discussion is that determining the incrementality of costs accurately becomes even more important for choosing and implementing pricing strategies once experience curve effects are taken into consideration. The execution lesson is also clear for pricing strategists: use pricing strategies to sell more and lower the per-unit costs proportionately to earn a higher profit on a lower price.

The declining incrementality of costs for pricing decisions

To make effective pricing decisions, the decision maker must consider not current or average costs but rather how costs will change on account of the pricing decision. The precise incrementality of costs matters to the pricing decision.

Applying the experience curve framework to incremental costs means that for any pricing decision, not only will incremental costs be lower than the average costs, but these incremental costs will decline when the pricing strategy results in more units sold; furthermore, this decline in incremental costs will accelerate as the pricing strategy promotes more sales. These relations support extreme-value pricing strategies that boost sales.

The profit boost of blowout price promotions

The first obvious implication of declining cost incrementality is that price promotions can be seen in an even more favorable light than when evaluated strictly through an incremental cost lens. Many managers and even many pricing strategists tend to view price promotions negatively. Cost incrementality means that the hurdle to make money on any price promotion is much lower than average cost considerations.

Declining cost incrementality goes even further, suggesting there will be an even more substantial profit boost from running blowout promotions that appear questionable on the surface but generate healthy profits in reality. There are literally countless examples of this principle. Here are two of them.

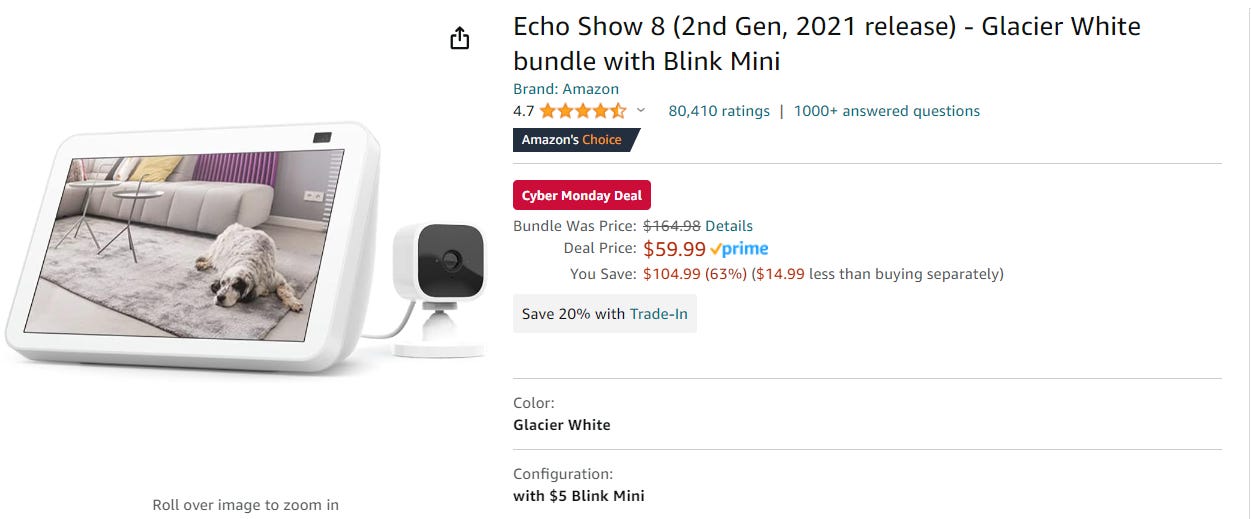

The first one is an Amazon Echo screen bundled with a Blink Mini that is priced for a 2023 Cyber Monday deal at $59.99, 63% off the regular prices. The second is a prix fixe menu for 2023 Houston Restaurant Weeks (HRW) for a three-course meal at Pappas Bros. Steakhouse for $48 (after deducting a $7 donation to the Houston Food Bank), approximately 45% off the regular price.

These promotions are blowout promotions because both offerings are very popular and sell easily at the respective high, regular prices. It is, therefore, fair to question how the sellers can afford to offer such good deals and why they would want to do so. On the surface, blowout promotions like these seem like a bad idea for the brands involved. However, the reality is that the incremental costs to cover these promotions are substantially lower (e.g., Pappas Bros. Steakhouse only has to cover the cost of food and other variable costs for the HRW promotion). The more attractive the deal, the more successful the promotion will be.

Blowout promotions that drive hordes of customers and raise unit sales substantially will drive the already low incremental costs even lower. As Izaret and Sinha point out, because semi-variable costs benefit more from scaling down the experience curve, the higher the component of semi-variable costs in the brand’s offering, the more pronounced the benefits of declining cost incrementality will be for that brand. Promotions that appear to make no sense on the surface and lead customers to ask, “How is the seller making money from this?” will actually be very profitable when seen through the lens of declining cost incrementality.

The virtue of low, all-in pricing

Another interesting implication of declining cost incrementality is that simple price structures that offer clearly excellent relative value to customers, fuel popularity and scale far down the fixed cost curve work really well. The famous French bistro, Le Relais de Venise l’Entrecôte is a case in point. It is one of the most renowned bistros in Paris, known for offering a very limited menu, comprising unlimited plates of delicious steak and frites for a remarkably low price. The New York Times described its business model back in 2009 when the restaurant opened a branch in New York City, as follows:

“It has no real menu to speak of. There is only salad and steak frites. Some wine to drink and a dessert after... And you know what? It’s terrific… Lacking restaurant experience, M. Gineste de Saurs [the founder] had limited ambition. He thought only to offer a salad to start, and then a grilled cut of sirloin the French call entrecôte (and which we call strip steak), with a rich, buttery sauce and a copious amount of fries. He took no reservations; you simply showed up and were seated. Those decisions turned out brilliantly. They were an assault on the tyranny of choice. The restaurant was instantly called by its meat name, not its geographical one: L’Entrecôte. Lines formed and have been there ever since, even as the family has broken into parts, and opened slightly different franchise versions of the restaurant all over the world…You can find better meat elsewhere, of course, but such satisfaction as you’ll find in a meal here is rarer by far.”

The price for this rare meal of all-you-can-eat steak and frites was $24 in New York City at the time. Prices have gone up since then. When it reopened recently in New York after a two-year Covid-induced hiatus, it raised the price of its unlimited steak, salad, and fries combo to $33.95. But still, it’s a fantastic price when comparable steakhouse dinners can easily cost five times as much.

As a general rule, I favor moderate complexity in price structures. But in the case of Le Relais de Venise l’Entrecôte, the extreme-value simplicity of the offering and the price draws hordes of customers sending it flying down the 50% fixed cost experience curve. The same type of experience-curve-driven declining cost incrementality that serves retailers like Costco and Aldi also serves niche businesses like Le Relais de Venise l’Entrecôte.

Two additional points are worth noting. First, like many successful brands that use the economic limitations induced by cost leadership as their brands’ defining characteristics that come to be beloved by customers (Southwest Airlines comes to mind here), the lack of menu choice, the fast service, the tables packed so close that “you’re practically swimming in your neighbor’s lap,” and the small portions of piping hot food have become powerful selling points for Le Relais de Venise l’Entrecôte, creating a unique, inimitable offering that people don’t mind waiting in line for. In a sense, the frugality-induced brand differentiation attracts more customers and amplifies the benefits of declining cost incrementality by extracting every ounce of usable capacity from the business’ fixed-cost and semi-variable cost resources. This is the virtuous cycle of experience-curve-driven declining cost incrementality.

On the negative side, however, the equilibrium created by successfully harnessing the declining cost incrementality is fragile. A brand capitalizing on declining cost incrementality with extreme-value pricing can only make money as long as all its assets are fully utilized. When the lines dwindle and the restaurant starts going empty, for instance, the highly strung economic logic also starts to break down as the business has to go into reverse, painfully climbing up the experience cost curves by scaling down. When Covid hit back in 2020, Le Relais de Venise l’Entrecôte was severely affected, even more so than other comparable restaurants. Its New York branch was closed for over two years, only opening again earlier this month. An extreme-value, all-in pricing model relies on extreme popularity to keep functioning smoothly.

Argote, L., & Epple, D. (1990). Learning curves in manufacturing. Science, 247(4945), 920-924.

Day, G. S., & Montgomery, D. B. (1983). Diagnosing the experience curve. Journal of Marketing, 47(2), 44-58; Ghemawat, P. (1985). Building strategy on the experience curve. Harvard Business Review, 63(2), 143-149.

Bruce Henderson, the founder of Boston Consulting Group, is credited with popularizing the experience curve in business applications (e.g., Boston Consulting Group, 1970; Henderson, 1984). Interestingly, the first documented application of experience curves goes further back to Wright (1936). References: Boston Consulting Group. (1970). Perspectives on Experience; Henderson, B. D. (1984). The application and misapplication of the experience curve. Journal of Business Strategy, 4(3), 3-9. Wright, T. P. (1936). Factors affecting the cost of airplanes. Journal of the Aeronautical Sciences, 3(4), 122-128. (The Wright paper is just a terrific read, and I hope to write a post about its brilliance soon).